5

225 Judicial Budgets: From Financial Outlays to Time-bound Outcomes

225 Judicial Budgets: From Financial Outlays to Time-bound Outcomes

Neha Sinha*

Abstract

In India, budgets for the judiciary are prepared based on recurring historical expenses, such as salaries, allowances, and minimum operational costs, without planning for capacity building or targeting desired outcomes. In this chapter, the authors argue that allocation and management of judicial budgets is directly correlated to the efficient operation of courts. As a case study, the authors present the budget of Maharashtra’s Law and Judiciary Department. The authors call for linking financial outlays in budgets to time-bound outcomes, through a framework of performance indicators, to improve judicial efficiency.

. . . . .

‘No matter how capable our judges, they cannot be effective unless adequate resources are provided,’ noted Michael L. Bender, Chief Justice, Colorado Supreme Court, United States of America, in his address on the State of the Judiciary to a Joint Session of the General Assembly in 2011.1 The judiciary in India, as in several developed and emerging economies, will confirm that the above quote applies universally.

Budgets are an integral component of any institution’s success, and the judiciary is no exception. Budgets for the judiciary in India have been based on historical recurring expenses, and have not involved a scientific planning process. A Ministry of Law consultation paper of 20012 noted, ‘In the past 50 years, there has been no proper allocation of funds commensurate with the increase in population, legal awareness, increase in legislation.’ The paper also noted, ‘The result is that there is, in terms of international Covenants and resolutions … a clear violation of the basic structure of the 226 Constitution and of the basic human rights resulting in an excessive “overload” of cases.’

Budgets for the judiciary have simply taken care of establishment costs, which essentially means that funds cover salary, allowances, and minimum operational costs of the judiciary, and do not provide for capacity building. In effect, budgets have merely reinforced the status quo. Central schemes are the favoured route for capacity addition. However, coordination and incentive structures are marred by the involvement of multiple agencies, without a clear demarcation of authority under the constitutional lists. In 1977, Entry 11-A was introduced in the Concurrent List of Schedule 7 of the Constitution of India by the 42nd Amendment Act of 1976. By this amendment, the subject ‘Administration of Justice: Constitution and organisation of all courts, except Supreme Court and High Courts’ was brought jointly under the purview of the centre and the states. However, a report by the Supreme Court of India on the National Court Management System showed that despite policies to promote equal participation, states were lacking in their contribution to court budgets.3

This chapter is organised in the following manner. The following section analyses the judicial budget for Maharashtra to understand certain contemporary budgeting practices in India. Thereafter, past schemes directed towards increasing capacity and budgetary capability within the judiciary are examined. Finally, performance indicators based on global best practices are discussed.

ANALYSING PRESENT–DAY BUDGETING PRACTICES IN INDIA

In this section, the judicial budget of Maharashtra is used as an illustration of existing budgeting practices in the country. Maharashtra, which is home to one of the oldest courts in India, is one of the most advanced states by state gross domestic product (GDP) in India.4 In comparison to other states, it also allocates a greater proportion of its yearly budget to the judiciary.5 Yet, it makes up for 3.46 per cent of India’s total pending cases, second only to Uttar Pradesh.6

This section considers the budget of the Department of Law and Justice (DOLJ) of Maharashtra and then uses the case of district courts in Maharashtra (from the DOLJ’s budget) to understand current budgeting practices in the state. The data has been collected from the Budget Estimation, Allocation and Monitoring System (BEAMS)7 of the Department of Finance under the government of Maharashtra.

The budget for the daily functioning of the justice machinery in Maharashtra is prepared by the DOLJ based in Mantralaya, Mumbai. The DOLJ is a technical department with two arms, administrative and legal. The administrative arm deals with matters concerned with the establishment at Mantralaya, the judiciary, and law officers among others, while the legal arm looks at drafting opinions, litigation, and conveyancing.8 In its current form, the various courts, quasi-judicial bodies, sub-departments, etc. under the DOLJ at Mantralaya, are categorised as ‘programmes’. Therefore, in terms of judicial budgets, this means that each level of the judiciary within the state is identified as a programme in itself. These programmes are subsumed within major budget heads which are representative of the main functions of the DOLJ of Maharashtra. The budget heads are:

1. Administration of justice: This budget head subsumes programmes related to all the levels of courts within the judicial hierarchy. It covers the establishment costs of courts within the state.

2 227 . Secretariat general services: This budget head includes the establishment costs for the Secretariat (at Mantralaya) and other administrative sub-departments within DOLJ.

3. Grants-in-aid to local bodies: This head includes funds from the central government for specific projects.

4. Capital outlay on public works: Under this head, funds are allocated for the acquisition of land and construction of new buildings—either for courts or for other departments related to adminstration.

5. Loans and advances:9 This budget head allocates money for purchase of computers, new building material, conveyance, and other immediate expenses.

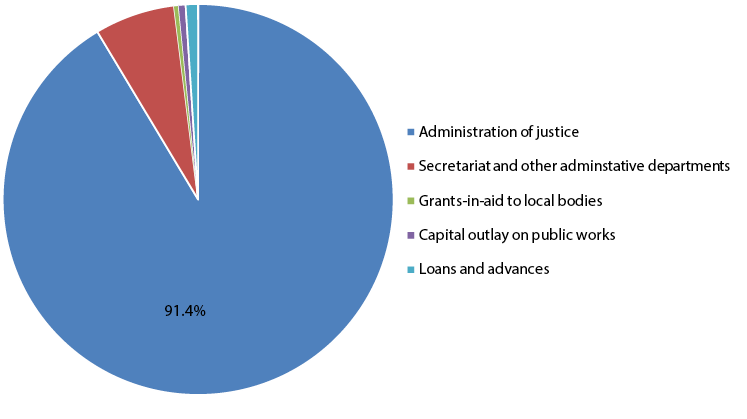

Figure 1 shows the composition of the DOLJ budget for 2016–2017. A total of Rs 1,919 crores was allocated to the department under the five budget heads discussed earlier .

FIGURE 1. Budget Allocation for DOLJ of Maharashtra, 2016–2017

Source: BEAMS and authors’ calculations.

Over 91 per cent of the DOLJ’s budget is spent on ‘administration of justice’. This budget head subsumes the allocation of funds to all courts in the judicial hierarchy of Maharashtra. A closer look at it is relevant for this chapter, to understand what it takes for the state to really deliver justice. For the purpose of this analysis, we focus on district and sessions courts, because the pendency in these courts10 is the highest among all courts in the judicial hierarchy. Pendency indicates the average number of days that a case spends in court awaiting resolution.

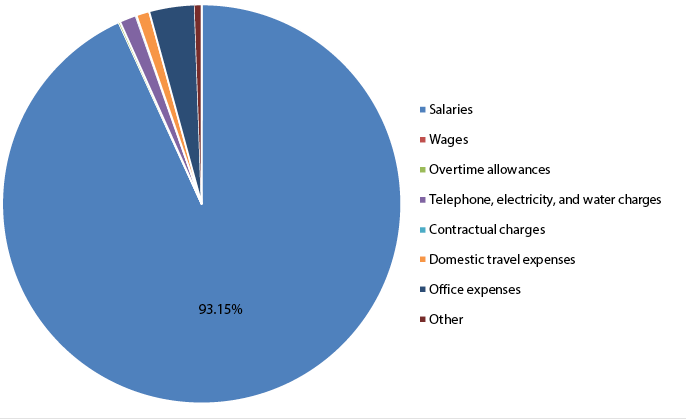

As per the DOLJ budget for 2016–2017, the total allocation under the ‘Civil, Sessions and Criminal Court’11 programme was Rs 1,177 crores. Of this amount, the district and sessions courts were allocated Rs 1,044 crores, and the distribution of funds can be seen in Figure 2.

FIGURE 2. Budget Allocation for District and Sessions Courts of Maharashtra, 2016–2017

Source: BEAMS and authors’ calculations

228 Over 93 per cent of the Rs 1,044 crores is spent on salaries of judges and other permanent staff working at the district and sessions courts. The remaining 7 per cent of the budget is allocated to other operating costs, such as office expenses (3.7 per cent), utilities (1.35 per cent), travel (1.05 per cent), etc. These costs leave no room for financing training, digital upgradation, or other capacity-building initiatives.

A LOOK AT PAST SCHEMES

Outcome-based budgets help deliver efficient services and increase accountability. However, our analysis of the DOLJ budget reveals that funds are mainly spent on salaries of judges and other permanent staff. This leaves a limited budget for systemic changes. Even though India has ostensibly moved to an outcome-based budget, this has not been adopted universally across states and different departments, and ‘the outcome budgets being produced by ministries are in fact, not outcome budgets, they are in effect “outlay budgets” only’.12 A careful assessment of budget allocations vis-à-vis the ultimate outcomes expected from the departments and public institutions is needed.

A World Bank report on modern budgeting practices for the judicial sector13 demonstrates that good budgets can substantially assist in raising the performance of the judicial sector. The report acknowledges that in the last decade, there has been an increase in awareness about the direct impact of legal and judicial reforms on economic and social development. The report notes that the concept has gained traction in emerging economies as well, and the key element of the judicial reform process has involved reorganisation and modernisation of the judiciary and the court system.

Digitisation is the favoured route to modernise the Indian judiciary. A study by Vidhi Centre for Legal Policy14 notes that various schemes for digitisation have been implemented since the early 1990s, of which, the most recent is the ‘e-Courts’ 229 project, which focuses on digitisation of the lower courts. Substantial success in the digitisation of the Supreme Court and High Courts has facilitated a higher rate of disposal of cases. However, the lower courts have experienced limited success in digitisation.

The study also notes that the budget for e-Courts has been repeatedly and drastically revised, indicating imprecisions in budgeting techniques. In 2007, the first phase of the e-Courts project was approved with a budget of Rs 442 crores, which was more than doubled and revised to Rs 935 crores in 2010. However, on the ground, it suffered from progressive under-spending. Subsequently, the budget for the second phase, estimated at Rs 1,670 crores, was approved with a significant delay.

OUTCOME BUDGETS AND PERFORMANCE INDICATORS

India is notorious for delayed justice, albeit not denied. There are more than 2.4 crore cases pending in the lower judiciary in India.15 At the end of 2015, there were more than 2.7 crore cases pending in the district courts, almost 39 lakh cases in the High Courts, and about 60,000 cases in the Supreme Court.16 This issue of high pendency is especially stark in the lower judiciary, with cases routinely taking more than 1,000 days to conclude.17 Cases which have not reached their timely conclusion not only stymie judicial efficiency, but tie up the litigants’ mental and physical time away from other productive activities. In Maharashtra, there are 2,566 judges at the district and taluk level to manage 32,76,689 pending cases.18 With a high pendency rate, the backlog in the system detracts from an efficient judiciary and imposes an economic cost on society, almost 0.5 per cent of GDP.19

Outcome-based budgets stress the importance of measuring various performance indicators to evaluate the effectiveness of financial allocations in improving a system.20 Outcome-based budgeting is a process in which the formulation of the budget centres on a set of defined objectives and expected outcomes. These outcomes help justify resource requirements, financial and otherwise, which are derived from and linked to such outcomes. The progress in achieving these outcomes is measured by specific performance indicators.21 Thus, the most important elements of an outcome-based budget include clearly defined objectives or outcomes, specific performance measures of such outcomes, linking of financial decisions to outcomes, and finally accountability based on these outcomes.22

The primary indicator used to assess the performance of the Indian judiciary is pendency. Other measures, such as workload of judges, cost of access to justice, and frequency of hearings, form a secondary part of the analysis.23 Official and public discourse on the subject of the performance of the judiciary also stresses on the issue of high pendency in Indian courts.24,25 It is a useful tool in understanding the workload and backlog of the court. In India, pendency is generally measured by court type and case type. Statutes and executive rules dictate the time frame within which a case must be disposed of, but in practice, these time limits are typically overshot, resulting in a backlog of cases in the judiciary.

Experts in the field26,27 acknowledge that focusing on pendency alone is a limited approach to evaluating the performance of the judiciary since it fails to capture ground realities, including vacancies. Vacancies in the judiciary adversely affect the rate of disposal of cases, since the workload of sitting judges correspondingly increases. Understaffing of administrative and clerical staff also leads to a backlog, which reflects the overall performance of the judiciary. Therefore, indicators such as pendency, 230 vacancy, workload, disposal rate, etc., are all interlinked in the way that they affect the effective functioning of the judiciary.

While these indicators look at the symptoms of inefficiency that need to be addressed imminently, they do not diagnose the depth of the problem. Developed economies, such as Singapore, United States of America, United Kingdom, and others, adopt a more nuanced approach using budgetary allocations. Budgeting, for them, includes myriad indicators that examine the performance of all the different departments within the judiciary, especially the adjudicating and administrative branches. The performance of these branches is used to determine allocations. They carefully review the experience of all the stakeholders of the judiciary, including adjudicators, administrators, and litigants, in order to determine the performance standards of the court system. Besides measuring performance using adjudication indicators,28,29 some courts even use administrative or management indicators and customer satisfaction indicators.30,31,32 Some of these measures include court user satisfaction, court file integrity, and employee engagement.33,34 The International Framework for Court Excellence recommends ‘eleven key measures across all court activity that reflects a high-level fair representation of a court’s overall performance’.35 These key measures include court-user satisfaction, access fees, case clearance rate, on-time case processing, pre-trial custody, court file integrity, case backlog, trial date certainty, court engagement, compliance with court order, and cost per case.

Moreover, the methodologies used to assess these indicators carefully review the qualitative effects of quantitative changes in the budget. They closely examine how current and proposed budgetary changes impact court performance. For example, the Missouri judiciary developed methodologies ‘to demonstrate how budget reductions would impact both revenues to the state and the courts’ ability to fulfil their mission’ and also attempted to ‘estimate the impact of investing in technology that will potentially improve efficiency and reduce costs’.36 Not only do they calculate how an increase in budgets would affect performance, but they also estimate how a decrease in budgets would affect performance standards.

It must also be recognised that in practice, the budgeting exercise is always a work in progress evolving alongside a changing governance structure. For instance, New Zealand37 embarked on performance budgets alongside reforms in the public sector and financial management in the late 1980s. The government conducts a periodic review of ‘output prices’ mutually agreed between departments and the treasury, rather than relying on input cost. The outcomes are easy to assess using a range of quantifiable outputs. For example, in the case of district courts, the outcome of safer community and fairer justice system is determined using parameters such as number of cases managed vis-à-vis annual target, levels of satisfaction amongst survey respondents towards case management, file preparation, and courtroom support against a target of meeting expectations for 80 per cent of the respondents. In a more recent evolution of the budgeting process, each department prepares an annual strategy document, ‘Statement of Intent’ and discerns how outcomes are arrived at from the policies and resourcing decisions of the government.

USING BUDGETS TO ACHIEVE OUTCOMES

Allocation and management of judicial budgets directly correlates to the efficient operation of courts. Similar to budgetary allocation heads, performance indicators should also fall within distinct categories, to guide efficiency in the judiciary and 231 foster accountability. In India, the court administrative staff (or clerical staff) prepares court budgets, which are then presented to the respective judges, before being sent to the state governments for their approval. Most judicial officers are not experts in budgeting practices and merely forward historic budgetary requirements for the following year.38

The success of budgets depends on linking financial outlays to time-bound outputs and outcomes, through performance indicators. The Union Budget of 2017–2018, in a marked departure from the historical methods of budget formulation, embarked on an outlay-output-outcome framework of formulating and tracking budgets for public schemes and projects under different ministries.39 The framework will measure ‘output’ as direct and measurable products of activities, expressed in physical terms or units, while ‘outcomes’ will be collective results of qualitative improvements brought about in delivery of services. The centrally sponsored schemes for development of infrastructure of subordinate courts and the central sector scheme of e-Courts Mission Mode Project Phase II, under the Ministry of Law and Justice, will be budgeted for and tracked under this new framework. While this is a step in the right direction, for it to become truly revolutionary, this framework needs to be developed for the entire judiciary.

Rationalising court budgets and monitoring their performance are two key factors in outcome budgets based on performance indicators. Under this approach, courts should prepare an annual budget proposal with holistic information, including the number of expected incoming cases for a year by case type, the available personnel and material resources, other court performance information, including length of proceedings, number of pending cases, expected number of judicial decisions, etc. and an estimated budget that is necessary to realise these expected outputs. At the end of a budget year the management of the courts should prepare an annual report, outlining the utilised budget and court performance.40 The framework should require, at the level of each court, regulations on the budget, which clearly demarcate phases, schedules, persons-in-charge, and goals that must be achieved at each stage. These regulations and the outcomes should be regularly updated and available publicly in order to monitor the process and foster accountability.41 The framework should also include measurement of performance indicators and a monitoring and evaluation system, among other things, implemented cohesively by all agencies involved.42 Looking at a limited set of indicators, particularly pendency, in a vacuum from other performance measures such as increase in litigation by enactment of new laws, court user satisfaction, etc., and pumping funding into misaligned budget heads will not ameliorate the state of the Indian judiciary.

In a data-scarce country such as India, it may be prudent to even set intermediate outcomes such as improving data quality and availability of data for seamlessly tracking the complete judicial procedure, towards achieving the final goal of judicial efficiency. Schemes meant for capacity development should have a sunset clause and strict timelines on fund utilisation. This will promote re-evaluation of their effectiveness and keep incentive structures in place for achieving outcomes. Targets that need to be met under each budget head must be outlined, refined, and regularly monitored, by court administrators and professional accountants and auditors, in order to optimise the utility of judicial budgets as well as the time and capabilities of judicial officers. A dynamic process of evaluating the needs of an effective judiciary, and aligning the budgets accordingly, is an important step towards achieving an efficient judiciary.

232 Notes

* The authors would like to thank Arushi Mishra and Aarti Seksaria for their able research and editorial assistance.

1. Michael L. Bender. 2011. ‘State of the Judiciary 2011’, Colorado Supreme Court, 14 January, available online at https://www.courts.state.co.us/Courts/Supreme_Court/State_of_Judiciary_2011.cfm (accessed on 27 September 2017).

2. National Commission to Review the Working of the Constitution. 2001. A Consultation Paper on Financial Autonomy of the Indian Judiciary. New Delhi: Government of India. Available online at http://lawmin.nic.in/ncrwc/finalreport/v2b2-1.htm (accessed on 27 September 2017).

3. National Court Management Systems. 2012. ‘Policy & Action Plan’, Supreme Court of India, 27 September, available online at http://www.sci.nic.in/ncmspap.pdf (accessed on 27 September 2017).

4. Ministry of Statistics and Programme Implementation. ‘Annual and Quarterly Estimates of GDP at Current Prices’, Government of India, available online at http://mospi.nic.in/data (accessed on 27 September 2017).

5. National Court Management Systems Committee, ‘Policy & Action Plan’.

6. National Judicial Data Grid. 2017. ‘Summary Report of Maharashtra’, Supreme Court of India, 13 June, available online at http://164.100.78.168/njdg_public/graphical/home_barchart_statewise.php (accessed on 27 September 2017).

7. Finance Department. 2017. ‘Budget Estimation, Allocation and Monitoring System: Without Public Account and Deduct Recovery Report for 2017-2018’, Government of Maharashtra, available online at https://beams.mahakosh.gov.in/Beams5/BudgetMVC/MISRPT/DepartmentExp1.jsp#J (accessed on 27 September 2017).

8. Law and Judiciary Department. ‘Performance Budget 2013-2014’, Government of Maharashtra, available online at https://www.maharashtra.gov.in/pdf/Budget/Law%20and%20Judiciary%20Department.pdf (accessed on 27 September 2017).

9. The source of loans and advances cannot be commented on with certainty. Loans and advances are generally used unplanned expenses and therefore work as a short-term fund source.

10. Press Information Bureau of India. 2016. ‘Pending Court Cases’, Government of India, 3 March, available online at http://pib.nic.in/newsite/PrintRelease.aspx?relid=137291 (accessed on 27 September 2017).

11. This includes money for criminal courts, Mumbai City Civil and Sessions Judges, and District Civil and Sessions Judges. Criminal courts were allocated Rs 72 crores and Mumbai City Civil Judges were allocated Rs 61 crores. See Finance Department. 2017. ‘Budget Estimation, Allocation and Monitoring System: Without Public Account and Deduct Recovery Report for 2016–2017’, Government of Maharashtra, available online at https://beams.mahakosh.gov.in/ (accessed on 27 September 2017).

12. Sanjeev Mishra. 2011. ‘Outcome Budgeting in India: The Need for Re-Engineering’, Journal of Defence Studies, April, pp. 38–48. Available online at www.idsa.in/system/files/jds_5_2_smishra.pdf (accessed on 27 September 2017).

13. David Webber. 2007. ‘Good Budgeting, Better Justice: Modern Budget Practice for the Judicial Sector’, The World Bank: Law and Development Working Paper Series No. 3, 1 January, available online at http://siteresources.worldbank.org/INTLAWJUSTICE/Resources/LDWP3_BudgetPractices.pdf (accessed on 27 September 2017).

14. Shalini Seetharam and Sumathi Chandrashekaran. 2016. eCourts in India: From Policy Formulation to Implementation. New Delhi: Vidhi Centre for Legal Policy. Available online at http://vidhilegalpolicy.in/reports-1/2016/7/7/ecourts-india (accessed on 27 September 2017).

15. National Judicial Data Grid. 2017. ‘Summary Report of India’, Supreme Court of India, 13 June, available online at http://164.100.78.168/njdg_public/main.php (accessed on 27 September 2017).

16. Editorial Board. 2015. ‘Court News’, Supreme Court of India, October–December, available online at http://supremecourtofindia.nic.in/courtnews/Supreme%20Court%20News%20Oct-Dec%202016.pdf (accessed on 27 September 2017).

17. DAKSH. 2015. ‘Understanding Pendency’, DAKSH, available online at http://dakshindia.org/understanding-pendency/ (accessed on 27 September 2017).

18. National Judicial Data Grid, ‘Summary Report of Maharashtra’.

19. Sudipto Dey. 2016. ‘State of Indian Judiciary: Rising Pendency of Cases and Workload of Judges’, Business Standard, 16 August, available online at http://www.business-standard.com/article/international/state-of-indian-judiciary-rising-pendency-of-cases-and-workload-of-judges-116081600024_1.html (accessed on 27 September 2017).

20. Pratap Ranjan Jena. 2013. ‘Outcome Budgets, The Real Thing’, Hindu Business Line, 29 March, available online at http://www.thehindubusinessline.com/opinion/columns/outcome-budgets-the-real-thing/article4562194.ece (accessed on 27 September 2017).

21. 233 Council of Europe. 2005. Results Based Budgeting: Manual, Version 3.1. Available online at http://www.coe.int/t/budgetcommittee/Source/RBB_SEMINAR/RBB_Manual_en.pdf (accessed on 27 September 2017).

22. Greg Hager, Alice Hobson, and Ginny Wilson. 2001. ‘Performance-Based Budgeting: Concepts and Examples’, Legislative Research Commission, 14 June, available online at http://www.lrc.ky.gov/lrcpubs/RR302.pdf (accessed on 27 September 2017).

23. Harish Narasappa and Shruti Vidyasagar (eds). 2016. State of the Indian Judiciary: A Report by DAKSH. Bengaluru: DAKSH and EBC.

24. Editorial Board. 2016. ‘Court News’, Supreme Court of India, April–June, available online at http://supremecourtofindia.nic.in/courtnews/2016_issue_2.pdf (accessed on 27 September 2017).

25. Press Trust of India. 2016. ‘Government, Judiciary Agree to Appoint Retired Judges in High Courts To Fight Pendency’, NDTV, 4 November, available online at https://www.ndtv.com/india-news/government-judiciary-agree-to-appoint-retired-judges-in-high-courts-to-fight-pendency-1621555 (accessed on 27 September 2017).

26. Interview with a presiding judge of a centrally sponsored tribunal, whose name is concealed on request of anonymity.

27. Dey, ‘State of Indian Judiciary’.

28. Cases filed per judge, cases resolved per judge, clearance rate, pending cases per judge, caseload per judge, congestion rate, time to resolve a case, number of judges, and costs.

29. Maria Dakolias. 1999. ‘Court Performance Around the World: A Comparative Perspective’, Yale Human Rights and Development Journal, 2(1): 87–142. Available online at digitalcommons.law.yale.edu/cgi/viewcontent.cgi?article=1009&context=yhrdlj (accessed on 27 September 2017).

30. On-time case processing, pre-trial custody, court file integrity, case backlog, trial date certainty, employee engagement, compliance with court orders, cost per case, court user satisfaction, and access fees.

31. Dan H. Hall and Ingo Keilitz. 2012. ‘Global Measures of Court Performance: Discussion Draft Version 3’, International Framework for Court Excellence, 9 November, available online at http://www.courtexcellence.com/~/media/Microsites/Files/ICCE/Global%20Measures_V3_11_2012.ashx (accessed on 27 September 2017).

32. Laurie Glanfield. 2016. ‘Enhancing the International Framework for Court Excellence: IFCE 2016 and Beyond’. Paper presented at the International Conference on Court Excellence, Singapore, 28–29 January. Available online at https://www.statecourts.gov.sg/Resources/Documents/ICCE%202016/3(ii)%20IFCE%202016%20and%20Beyond_Glanfield_2016070716111647.pdf (accessed on 27 September 2017).

33. Hall and Keilitz, ‘Global Measures of Court Performance’.

34. Carol R. Flango, Amy M. McDowell, Charles F. Campbell, and Neal B. Kauder. 2010. Future Trends in State Courts 2010. Williamsburg, VA: National Center for State Courts, 2010. Available online at http://ndcrc.org/sites/default/files/future_trends_2010.pdf (accessed on 27 September 2017).

35. Glanfield, ‘Enhancing the International Framework for Court Excellence’.

36. Flango, et al., Future Trends.

37. David Webber. 2007. ‘Good Budgeting, Better Justice: Modern Budget Practice for the Judicial Sector’, The World Bank: Law and Development Working Paper Series No. 3, 1 January, available online at http://siteresources.worldbank.org/INTLAWJUSTICE/Resources/LDWP3_BudgetPractices.pdf (accessed on 27 September 2017).

38. National Court Management Systems, ‘Policy & Action Plan’.

39. Department of Economic Affairs. 2017. Output Outcome Framework for Schemes 2017–18. New Delhi: Government of India. Available online at http://dea.gov.in/sites/default/files/OutcomeBudgetE2017_2018.pdf (accessed on 27 September 2017).

40. Pim Albers. ‘Performance Indicators and Evaluation for Judges and Courts’, Council of Europe, available online at http://www.coe.int/t/dghl/cooperation/cepej/events/OnEnParle/MoscowPA250507_en.pdf (accessed on 27 September 2017).

41. Costel Todor. ‘Study on the Recent Practice of Funding the Judicial System, Taking into Account International Practices of Funding the Judicial System’, USAID and Rule of Law Institutional Strengthening Program, November, available online at http://crjm.org/wp-content/uploads/2013/11/Judicial-budgeting-in-MD.pdf (accessed on 27 September 2017).

42. Jena, ‘Outcome Budgets’.

———