Note: Figures considered are before the appointment of 35 additional members in April 2015. .

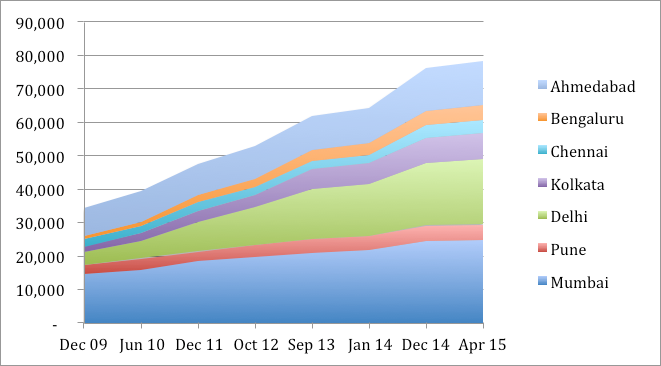

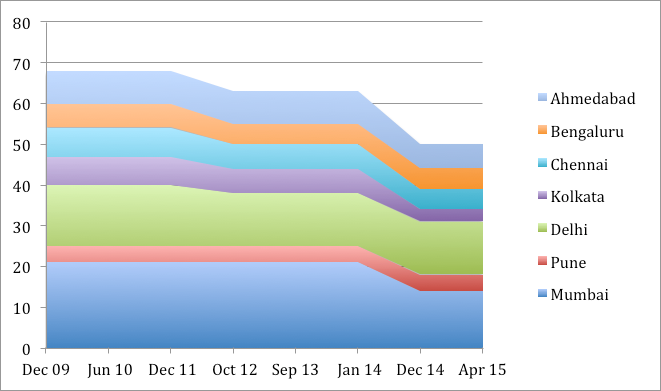

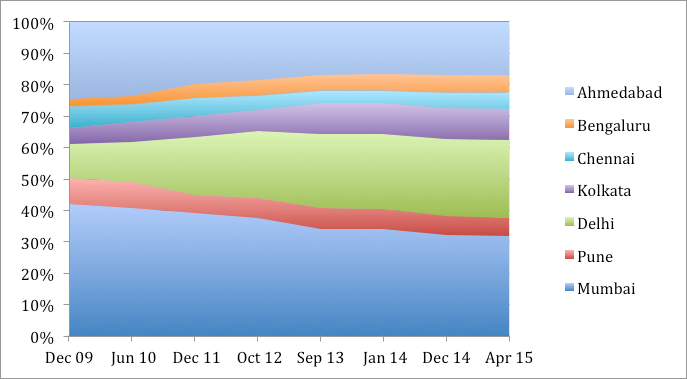

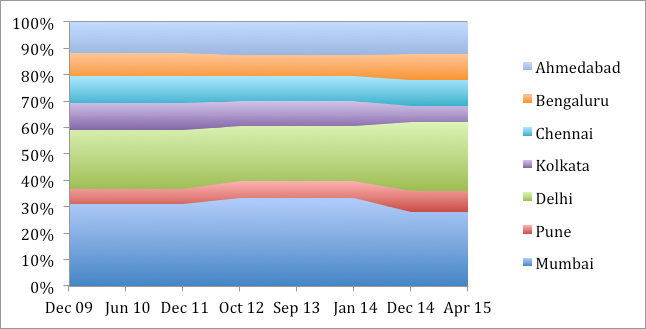

A review of the trends illustrated in Figures 1–4 (based on the information in Tables 1 and 2) leads one to note some significant points:

- Pendency in Delhi has increased massively (almost five times), while the number of members has remained almost constant.

- Pendency in Bangalore has also increased (more than in Delhi in percentage terms, but that is due to the low base), while here too, the number of members has remained almost constant.

- Pendency in Kolkata has also seen a huge spike (almost four-and-a-half times), and the number of members has reduced, albeit only in the last two years.

The recent appointment of additional members is definitely behind the curve, that is, it happened much after pendency increased significantly. While it may have led to an increase in the overall strength of members at the ITAT, city-wise appointments need to be on a rational basis so that more resources are allocated to those locations with greater pendency. If such metrics had been constantly monitored by civil society, and action taken based on the disclosed findings, pendency may have been at manageable levels.

Paucity of Data

However, as the discerning reader would have observed, one cannot draw satisfactory conclusions about the functioning of the ITAT from the data available. This is because of paucity of publicly available data. An institution as important as the ITAT must be assessed by civil society, just as any other institution of governance.

In this aspect the ITAT is not alone. There is, in general, paucity of information regarding the functioning of the judiciary in our country. Being one of the three pillars on which democracy stands, and arguably the strongest of the three, the judiciary should be subject to as much assessment as the other two, the legislature and the executive. Civil society needs to develop metrics and scorecards to measure the functioning of the judiciary. Such an exercise would help immensely in identifying changes required to legal processes, or even the law itself.

‘Rule of Law’ Project

A significant step in this direction is being taken under the ‘Rule of Law’ project by DAKSH, a Bangalore-based organisation, whose primary objective is putting together data about the Indian judicial system. Once the data compilation is completed and made available publicly, many interesting aspects of the working of our courts can be studied in detail. This quantitative and empirical approach should lead to informed public debate about judicial performance in the country, with a view to finding meaningful and sustainable solutions.

As an illustration, Figure 5 shows the average rate of disposal of some types of cases during 2014 and the first quarter of 2015 in the High Court of Karnataka:

Figure 5: Average Time Taken for Disposal

Case Type | Average Disposal (Years) |

| Writ petition | 2.12 |

Writ appeal | 2.48 |

Sales tax/VAT revision petition | 2.72 |

Sales tax/VAT appeal | 3.13 |

Income tax appeal | 3.74 |

Source: Daksh

The next step could be further analysis through comparing metrics across different courts, over various periods of time, other case types, and examining the root cause for differences.

For instance, if more information were available about the ITAT, one could have delved into questions such as:

- What is the average time taken to dispose of an appeal, from the date of filing to the date of final disposal?

- How do various benches compare in terms of disposal and pendency?

- What is the distribution of different types of cases? For example, relating to international tax, personal tax, tax holidays, etc.

Such a quantitative analysis would be just the beginning for further qualitative review.

A foundation for an empirical analysis of judicial performance is only now being laid and not enough can be said about its significance. One hopes that this will lead to the establishment of a framework for measuring the performance of our tax courts.

Table 1. City-wise Split of Cases Pending before the ITAT

| December 2009 | June 2010 | December 2011 | October 2012 | September 2013 | January 2014 | December 2014 | April 2015 | |

| Mumbai | 14392 | 16007 | 18611 | 19840 | 21000 | 21827 | 24448 | 24708 |

| Pune | 2849 | 3203 | 2780 | 3368 | 4100 | 4116 | 4674 | 4620 |

| Delhi | 3766 | 5081 | 8767 | 11260 | 14769 | 15377 | 18557 | 19582 |

| Kolkata | 1709 | 2422 | 3251 | 3563 | 6080 | 6384 | 7511 | 7743 |

| Chennai | 2311 | 2198 | 2622 | 2380 | 2378 | 2528 | 3769 | 3913 |

| Bengaluru | 831 | 1144 | 2208 | 2713 | 3256 | 3514 | 4370 | 4481 |

| Ahmedabad | 8495 | 9210 | 9369 | 9746 | 10370 | 10621 | 12775 | 13243 |

| Others | 12354 | 14125 | 14764 | 16118 | 19062 | 20039 | 24316 | 25691 |

| Total | 46707 | 53390 | 62372 | 68988 | 81015 | 84406 | 100420 | 103981 |

Table 2. Number of Members on Various ITAT Benches

December 2009 | June 2010 | December 2011 | October 2012 | September 2013 | January 2014 | December 2014 | April 2015 | |

Mumbai | 21 | 21 | 21 | 21 | 21 | 21 | 14 | 14 |

Pune | 4 | 4 | 4 | 4 | 4 | 4 | 4 | 4 |

Delhi | 15 | 15 | 15 | 13 | 13 | 13 | 13 | 13 |

Kolkata | 7 | 7 | 7 | 6 | 6 | 6 | 3 | 3 |

Chennai | 7 | 7 | 7 | 6 | 6 | 6 | 5 | 5 |

Bengaluru | 6 | 6 | 6 | 5 | 5 | 5 | 5 | 5 |

Ahmedabad | 8 | 8 | 8 | 8 | 8 | 8 | 6 | 6 |

Others | 34 | 34 | 34 | 24 | 24 | 22 | 17 | 17 |

Total | 102 | 102 | 102 | 87 | 87 | 85 | 67 | 67 |

Note: Figures considered are before the appointment of 35 additional members in April 2015.

The views expressed in this article are solely those of the author’s and they do not represent the views of DAKSH.