4

163 Government Litigation: A Study of Tax Appeals in Karnataka and Gujarat

163 Government Litigation: A Study of Tax Appeals in Karnataka and Gujarat

Abstract

Government litigation is often blamed for the huge pendency of cases in courts. However, precise numbers to back up this claim are elusive. A study of a specific type of government litigation, namely tax appeals, in the High Courts, can provide some insight into how a particular government approaches a certain kind of case. To do this, the author compares the approaches of the union government and state governments of Karnataka and Gujarat in filing tax appeals before the High Courts of Karnataka and Gujarat respectively, to determine whether any patterns emerge from the data to indicate how many of the government’s cases may be characterised as ‘frivolous’. The author finds that the central government is more litigious than state governments in terms of filing tax appeals, and suggests that it needs to immediately re-think its approach to tax litigation.

. . . . .

It is a truism that in India, ‘the government’ is the single largest litigant in the country. Those concerned about the pendency of cases and delays in cases in India tout this as a possible cause, dropping (unverifiable) figures which suggest that government litigation constitutes anywhere between 50 per cent and 7 per cent of all cases in the system.1 One recent ‘study’ by the Ministry of Law suggested that central and state governments filed 46 per cent of all cases pending in the judicial system,2 though it is unclear what the methodology followed was to arrive at that number. There is also no single, cogent definition of ‘government litigation’. It could mean cases filed by the government, cases filed against the government, or both. Assuming the widest definition possible — cases filed by and against the government — by itself does not tell us anything useful 164 or actionable in the context of delay and pendency. At the most basic level, it might mean that government litigation is a significant contributor to the ‘supply’ of litigation in India. However, this raises further questions, such as:

1. Which ‘government’ or set of entities are being referred to here?

2. How much does this entity (or do these entities) contribute to litigation supply?

3. How much of it is unnecessary or burdening the court?

What is commonly called the ‘government’ has many shades and aspects to it legally. India, being a federal polity, has both central and state governments, apart from the local self-government bodies, that is, the panchayats and municipalities. All these bodies act independently, having been given independent powers and functions under the Constitution of India and relevant statute.

Likewise, there are several bodies set up by the Constitution or a statute — these include universities, regulatory bodies, commissions, and others. They function independently of the central or state government. They may be ‘state’ for the purposes of Article 12 of the Constitution3 or ‘authorities’ for the purposes of Article 226,4 but that does not make them ‘government’ as this is a clearly defined category even under the Constitution.

Constitutionally, the ‘government’ in India is the executive wing of the state — the bureaucracy and the ‘political executive’ which is empowered to exercise all executive functions under the Constitution.5 It is this body, both at the central and the state level that I will focus on for the purpose of this study.

This helps us arrive at a narrower definition of government litigation: all cases filed by or against these bodies, namely the central government, the state governments, and the governments of the union territories in the courts of the country. Such cases are filed at all levels, from the magistrates’ courts to the Supreme Court, including tribunals of various sorts, set up by the state and central governments.

In any nation that abides by the rule of law, it is only just and fair that citizens see the court as an institution to remedy any failings or shortcomings or illegalities committed by the government. Likewise, the state is required to abide by the due process of law in punishing people or imposing civil or criminal penalties upon them, and this includes providing a fair hearing before a neutral and independent court. It is therefore highly likely that government litigation will form a significant part of the judiciary’s workload in any nation that follows the rule of law.

That being said, how an individual or a private entity approaches or choose to undertake litigation is not the same as the manner in which the government chooses to undertake litigation. An individual chooses to undertake litigation because it directly affects her, likewise a private entity. It is, however, not always obvious as to why the government undertakes litigation in every case. Theoretically, the government does not just act in its own interest but also in the larger public interest. Second, the person making the decision to litigate is more removed from the consequences of the litigation in the case of the government than with private entities or individuals. Third, the resources available to the government vastly outstrip those available to individuals or entities by many orders of magnitude (with a few exceptions).

The effect of this is that it is possible that the government, as a litigant, might be acting in an irresponsible manner by filing a large number of frivolous cases. This may not necessarily be in bad faith. Rather, this may be because of the existence of 165 a perverse set of incentives (arising out of the factors mentioned above) which result in the government filing cases in which it has no hope of winning, but ends up overburdening the court system. Whether a case is frivolous depends on the context — an overarching definition that covers everything from simple money suits to constitutional cases is neither necessary nor desirable. What makes a suit frivolous is very different from what makes a tax appeal frivolous and entirely different from what makes an appeal from a tribunal frivolous.

Given a case type and a subject matter, how then do we assess if the case is ‘frivolous’? One answer is to see if the court, in dismissing or disposing the case within a few months of filing, has held it to be ‘frivolous’ or made an observation to that effect. This methodology was adopted by Vidhi Centre for Legal Policy in their report titled Inefficiency and Judicial Delay: Insights from the Delhi High Court where they studied cases filed in the High Court of Delhi between 2011 and 2015.6 From a representative sample of cases that they examined, they found that about 4 per cent of the cases were ‘frivolous’ by this definition. However, the authors did point out that this number seems too low and it is possible that a larger number of cases are in fact frivolous but that fact has not been recorded by court. A different definition of ‘frivolity’ therefore needs to be found.

Frivolity could be defined in a manner that accounts for the obvious nature of such frivolity. A case which has no chance of succeeding is usually one which does not even require the other side to rebut factual or legal submissions. The lack of merits is so obvious, it results in the case being dismissed in limine. This should be distinguished from the dismissal of a special leave petition by the Supreme Court or any case where the court’s jurisdiction is a matter of discretion, not a right. This definition will also exclude those where the court dismisses the case on a technical ground such as (lack of) jurisdiction.

The problem therefore may be framed thus: are cases being filed by the government that need not have been filed, and thus, constitute a waste of the court’s time and resources?

One way to define frivolous government litigation would be to look at where the government has a choice between filing and not filing a case, and even when the judgment is highly unlikely to go in its favour legally, the government proceeds to file the case. One such type of case, which has been commented upon, is in relation to appeals by the government against orders relating to pensions and service conditions of serving and retired armed forces personnel passed by the Armed Forces Tribunal. Data obtained by the Vidhi Centre for Legal Policy showed that in 2014, of the 924 appeals filed against the orders of the Armed Forces Tribunal, 890 (or nearly 96.3 per cent) were filed by the Ministry of Defence. Of these, more than 96.7 per cent were dismissed in the first hearing itself, suggesting that the Supreme Court did not find any substantial question of law involved in the case (as required by the Armed Forces Tribunal Act, 2007). One can safely say perhaps, that the Ministry was not justified in filing most of these appeals.

Another area of government litigation that has received much attention has been the filing of appeals by the tax department. As of December 2011, Rs 1.84 trillion of central government revenues in income tax were held up in nearly 65,998 tax appeals pending at all levels.7 This figure has been increasing over the years, and at first blush, seems to suggest an inefficient judiciary. A deeper examination, however, reveals that the central government loses nearly 70 per cent of the cases and that most of this money is not recoverable anyway. It would therefore seems that it is the government that is passing the buck on to the courts and adding to their burdens. Tax appeals prima facie seem to provide a good example of wasteful government litigation, and require to be studied further to see 166 if this still holds true. Tax litigation being a subject matter where both central and state governments in India are likely to file a substantial number of cases, it would be possible to compare and contrast the way in which these governments approach such litigation. This should provide understanding on whether both central and state governments suffer from the same pathology when it comes to tax litigation.

The bulk of tax litigation is simply a question of money, and for both the revenue and the citizen, the incentive is theoretically the same: is the expense of litigation worth the money I am going to recover?

Even where the tax outgo or revenue intake is on a recurring basis, the calculation is the same. An assessee is likely to be affected by an adverse judgment in years to come, just as the revenue is likely to be affected vis-à-vis the assessee in future years. If a case has larger implications beyond the assessee for the revenue (if it loses the case), it also enjoys a power that the assessee does not: the power to amend the law. Theoretically, the assessee and the government should be making the same kind of calculation in deciding whether to file an appeal against an adverse judgment — what are my chances of success in recovering the amount at stake? Whether that happens in reality is what I will analyse in this chapter.

Examining data available in the DAKSH database on the High Courts of Gujarat and Karnataka, this chapter looks to answer the following questions:

1. Is the central government more likely to file appeals in tax cases, in the High Court, than assessees?

2. Is the state government more likely to file appeals in tax cases, in the High Court, than assessees?

3. Inter se state governments, which government is more likely to pursue tax appeals?

METHODOLOGY

For the purpose of analysis in this chapter, cases filed from 2011 to 2015 have been chosen. These cases have been chosen both from the DAKSH database and supplemented, where possible, with cases from the websites of the High Courts of Karnataka and Gujarat. These High Courts have been chosen based on the depth of detail on these High Courts available in the DAKSH database. Coincidentally, they also happen to be among the five largest state economies in India, and are therefore likely to have a sizeable sample of cases to study.

To narrow down categories of tax cases and ensure that comparison takes place on a like-for-like basis, income tax cases of the central government, and sales tax or value added tax (VAT) cases for state governments, have been taken into account. The High Court exercises reasonably similar functions in both cases — examining whether the order of the tribunal is justified in law, without a full re-examination of the facts already established.

Whereas the High Court of Karnataka has a separate category for income tax and sales tax appeals, all of them are clubbed together as ‘Tax Appeals’ in the High Court of Gujarat, with case categories distinguishing between income tax and sales tax cases.

The data collected here is not comprehensive of all tax cases filed in this duration in either the High Court of Karnataka or the High Court of Gujarat. The DAKSH database relates to cases which have been listed for hearing after 2014 and, therefore, will not necessarily contain details of all the cases which have been filed in the five-year 167 period. However, some data about the cases filed in this period can be gleaned from the websites of the High Courts themselves and this has been done wherever possible.

There is one anomaly in the data which needs to be accounted for. For the years 2011 and 2012, there seem to have been hardly any cases filed in the High Court of Gujarat on VAT. It is unclear exactly what caused this. A possible explanation is that the Gujarat Value Added Tax Tribunal was non-functional during this period, resulting in no cases being decided, and hence no appeals being filed in the High Court.

JURISDICTION

Under the Income Tax Act (IT Act), 1961, an appeal can be filed against the order and judgment of the Income Tax Appellate Tribunal to the jurisdictional High Court. Only an ‘aggrieved party’ can file an appeal against an order of a lower forum to a higher one. An aggrieved party is one whose civil rights have been disturbed in some way by the order and judgment of the lower court.

This being a second appeal, the requirement is that an appeal to the High Court should involve a ‘substantial question of law’. A substantial question of law has been interpreted by the Supreme Court to mean a question of law which has not been finally settled by any superior court and substantially affects the rights of the parties to the case.8 Similarly, Section 78 of the Gujarat Value Added Tax Act (GVAT Act), 2003, which was amended in 2006 by the Gujarat Value Added Tax (Amendment) Act, 2006, allows for aggrieved parties to file appeals before the Gujarat High Court from the orders of the Gujarat Value Added Tax Tribunal on a ‘substantial question of law’. Since the phrasing is almost identical to the IT Act, it would have the same connotation.

The Karnataka Value Added Tax Act (KVAT Act), 2003, on the other hand, grants a limited right of revision against the orders of the Karnataka Value Added Tax Tribunal and a right to appeal against the orders of the Commissioner or the Additional Commissioner acting in a quasi-judicial capacity. Under Section 65 of the KVAT Act, a revision petition can be filed against an order of the Tribunal in the High Court, where a question of law has not been decided or decided incorrectly. This is a narrow jurisdiction, but in some ways akin to the appeal under the IT Act and GVAT Act. For the purposes of this study, revision applications have also been incorporated and studied to ensure that there is uniformity among the types of cases being considered.

One caveat is necessary here. The Central Board for Direct Taxes has periodically issued instructions to the income tax department to limit tax litigation. It has done this by limiting appeals in cases where the amount at stake is below a certain threshold. The latest circular (Circular No. 21 of 2015), for instance, prescribes Rs 10,00,000 as the minimum limit for an appeal to be filed before the ITAT, Rs 20,00,000 as the limit for High Courts, and Rs 25,00,000 as the limit for the Supreme Court. Given that this direction was issued 2015, it may have had some impact on the numbers presented below. Presently, there does not seem to be any equivalent for the states.

ANALYSIS OF DATA

Table 1 compares the number of appeals filed in income tax cases, by the revenue and assessees, in the High Courts of Karnataka and Gujarat.

TABLE 1. Comparison of Appeals Filed by Revenue and Assessees in the High Courts of Karnataka and Gujarat in Income Tax Cases

|

Karnataka |

Gujarat |

|||||

|

Year |

Government appeals |

Private appeals |

Ratio |

Government appeals |

Private appeals |

Ratio |

|

2011 |

66 |

11 |

6.00 |

829 |

178 |

4.66 |

|

2012 |

214 |

67 |

3.19 |

509 |

167 |

3.05 |

|

2013 |

304 |

55 |

5.53 |

742 |

113 |

6.57 |

|

2014 |

234 |

280 |

0.84 |

579 |

120 |

4.83 |

|

2015 |

636 |

157 |

4.05 |

455 |

58 |

7.84 |

|

Total |

1,454 |

570 |

3,114 |

636 |

||

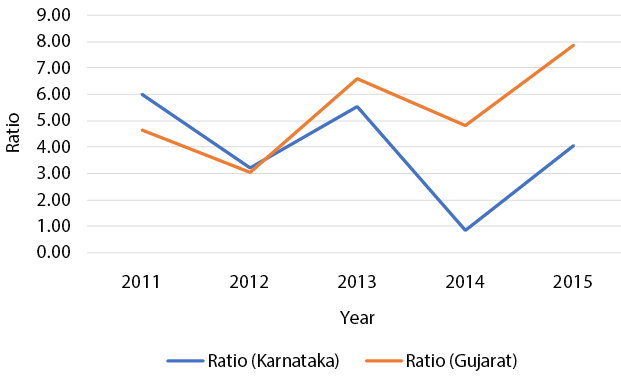

168 One key point of difference to note here is that while the details of cases in the High Court of Karnataka have been taken from the DAKSH database, details of the cases in the High Court of Gujarat have been taken from the DAKSH database, and supplemented by information on the website of the High Court of Gujarat. Nonetheless, we see a fairly consistent pattern throughout — government appeals far outstrip appeals by assesses. Figure 1 shows the comparison between the ratio of government to assessee appeals in the two High Courts.

FIGURE 1. Comparison of Ratio of Government to Assessee Appeals in the High Courts of Karnataka and Gujarat

Table 2 compares the number of appeals or revision petitions filed under VAT laws, by state governments and assessees, in the High Courts of Karnataka and Gujarat.

TABLE 2. Comparison of Appeals/Revision Petitions filed by State Governments and Assessees under VAT Laws in the High Courts of Karnataka and Gujarat

|

Karnataka |

Gujarat |

|||||

|

Year |

Appeals filed by government |

Appeals filed by assessees |

Ratio |

Appeals filed by government |

Appeals filed by assessees |

Ratio |

|

2011 |

18 |

36 |

0.50 |

1 |

13 |

0.08 |

|

2012 |

21 |

46 |

0.46 |

3 |

3 |

1.00 |

|

2013 |

2 |

38 |

0.05 |

72 |

63 |

1.14 |

|

2014 |

14 |

50 |

0.28 |

70 |

87 |

0.80 |

|

2015 |

22 |

49 |

0.45 |

142 |

63 |

2.25 |

|

Total |

77 |

219 |

288 |

229 |

||

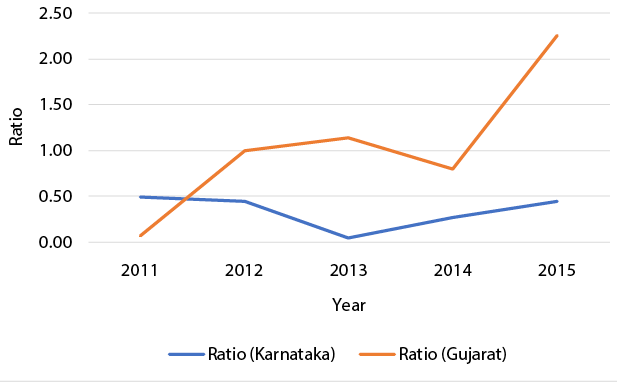

169 In contrast to the income tax appeals, appeals in VAT cases seem to be filed at least as many times, if not more often, by assessees rather than state governments. Data for a few years appears anomalous — 2013 for Karnataka and 2011 and 2012 for Gujarat — insofar as the absolute number of appeals are concerned, and there are no obvious explanations for this, but in general, the government of Karnataka seems to file fewer appeals on average compared to the government of Gujarat. What this could be attributed to is not immediately obvious, and requires greater in-depth research into the manner in which assessments are carried out in the respective states. The year 2015 is the sole exception in this data, where the number of appeals filed by the state government seems to vastly outstrip the number of appeals filed by the assessee.

Figure 2 shows the comparison between the ratio of government to assessee appeals in the two High Courts filed under VAT laws.

FIGURE 2. Comparison of Ratio of Government to Assessee Appeals in the High Courts of Karnataka and Gujarat

170 Tables 3 and 4 compare the pendency of appeals in income tax and VAT cases respectively in the two chosen High Courts, in terms of actual numbers as well as the ratios of government to assessee appeals.

TABLE 3. Comparison of Pendency of Appeals in Income Tax Cases

|

Karnataka |

Gujarat |

|||||

|

Year |

Appeals filed by government, still pending |

Appeals filed by assessees, still pending |

Ratio |

Appeals filed by government, still pending |

Appeals filed by assessees, still pending |

Ratio |

|

2011 |

60 |

2 |

30.00 |

396 |

119 |

3.33 |

|

2012 |

160 |

44 |

3.64 |

195 |

108 |

1.81 |

|

2013 |

194 |

26 |

7.46 |

261 |

53 |

4.92 |

|

2014 |

179 |

258 |

0.69 |

247 |

82 |

3.01 |

|

2015 |

614 |

149 |

4.12 |

196 |

32 |

6.13 |

|

Total |

1,207 |

479 |

1,295 |

394 |

||

A comparison of pendency of appeals filed in each year (as of the date on which the data was collected), shows that the pendency of cases does not seem to be dramatically different between government and assessee appeals. However, far more government cases in the High Court of Karnataka seems to be pending vis-à-vis assessee appeals; likewise, in the High Court of Gujarat.

TABLE 4. Comparison of Pendency of Appeals in VAT Cases

|

Karnataka |

Gujarat |

|||||

|

Year |

Government pending |

Private pending |

Ratio |

Government pending |

Private pending |

Ratio |

|

2011 |

2 |

5 |

0.40 |

0 |

0 |

0.00 |

|

2012 |

0 |

12 |

0.00 |

0 |

1 |

0.00 |

|

2013 |

2 |

38 |

0.05 |

13 |

7 |

1.86 |

|

2014 |

10 |

42 |

0.24 |

5 |

20 |

0.25 |

|

2015 |

22 |

48 |

0.46 |

17 |

17 |

1.00 |

171 Similar to income tax appeals, the ratio of pending government appeals to assessee appeals does not seem to be dramatically different from the ratios in which they are filed.

CONCLUSIONS

Some key conclusions can be summarised from the above data:

1. The central government tends to file far more income tax appeals than assessees (nearly four times as many) in the High Courts of Karnataka and Gujarat put together.

2. The government of Karnataka, during the period for which data was examined, filed far fewer tax appeals and revisions than assessees did in the same period — a ratio of 0.35 for the five-year period. On the other hand, the government of Gujarat filed more appeals than assessees, but only by a factor of 1.26.

3. With reference only to assessees, the central government seems far more litigious than the state governments when it comes to tax appeals.

4. As far as pendency is concerned, there does not seem to be an observable difference between government appeals and appeals by assessees.

What explains the dramatic differences between the litigiousness of the state and the central governments in tax matters?

One possible explanation is the fact that the income tax department seems to lose a lot more cases in the ITAT. One report estimates that the revenue loses 80 per cent of all tax cases in the tribunals.9 This might explain why the revenue files far more appeals in the High Courts than the state governments in tax cases. Comparable figures are not available for the state governments of Gujarat and Karnataka to confirm this. This also raises a further question: why does the ITAT decide so many cases in favour of the assessee?

When contrasted with the fact that in the appellate layer immediately below that, the Commissioner of Income Tax (Appeals), the Revenue ‘wins’ 75 per cent of the cases, it does not seem so absurd. This is also because the CIT(A) is a serving officer of the Revenue and is more likely to side with the Revenue in an appeal from the order of the assessing officer. There is perhaps a need to re-look this level of appeal and what purpose it serves.

172 In the Supreme Court data collected by the Vidhi Centre for Legal Policy, of 732 cases filed by the income tax department in 2014, 216 or 29.51 per cent had been dismissed in limine.

There seem to be underlying problems with the way the income tax department approaches litigation that cannot be fixed simply by setting monetary limits to filing of appeals.

While the number of tax cases does not suggest that they are a significant burden on the two High Courts in question, it is possible that in other High Courts, such as the High Courts of Delhi and Bombay, where the volume of tax litigation is much higher,10 the government’s approach to litigation may in fact be leading to greater delay.

At the moment, the data is not sufficient to check if the cases that are being filed are frivolous, but as DAKSH collects more data, this may be possible to address. For the moment however, one conclusion that stands from the data is that the central government needs to immediately re-think its approach to tax litigation.

Notes

1. Ameen Jauhar. 2016. ‘Time to Move Towards a New Litigation Policy’, The Hindu, 18 November, updated on 2 December 2016, available online at http://www.thehindu.com/todays-paper/tp-opinion/Time-to-move-towards-a-new-litigation-policy/article16543929.ece (accessed on 28 September 2017).

2. Pradeep Thakur. 2017. ‘46 per cent of Three Crore Pending Cases Filed by Centre, States’, The Times of India, 22 June, available online at http://timesofindia.indiatimes.com/india/46-of-three-crore-pending-cases-filed-by-centre-states/articleshow/59261258.cms (accessed on 28 September 2017).

3. See Pradeep Kumar Biswas v. Indian Institute of Chemical Biology, (2002) 5 SCC 111 on what is ‘state’ for the purposes of Art. 12 of the Constitution.

4. See K.K. Saksena v. International Commission on Irrigation & Drainage, (2015) 4 SCC 670.

5. Art. 53 in the context of the union government and Art. 154 in the context of the state government.

6. Nitika Khaitan, Shalini Seetharam, and Sumathi Chandrashekharan. 2017. ‘Inefficiency and Judicial Delay: New Insights from the Delhi High Court’, 29 March, available online at https://vidhilegalpolicy.in/reports-1/2017/3/29/inefficiency-and-judicial-delay-new-insights-from-the-delhi-high-court (accessed on 28 September 2017).

7. Kian Ganz. 2015. ‘Untangling the Complex Web of Tax Laws’, Livemint, 2 December, available online at http://www.livemint.com/Politics/B3w8aqk5fdu3lBQasJhHoN/Untangling-the-complex-web-of-tax-laws.html (accessed on 28 September 2017).

8. Chunilal V. Mehta and Sons Ltd. v. Century Spg. and Mfg. Co. Ltd., AIR 1962 SC 1314.

9. Remya Nair. 2014. ‘CBDT Sets up Panel to Look into Dispute Resolution’, 14 July, available online at http://www.livemint.com/Politics/jQiziSTfvMgRo5rOsuNDYI/Finance-ministry-sets-up-panel-to-reduce-tax-litigations.html (accessed on 28 September 2017).

10. Between 2011 and 2015, the High Court of Delhi saw 4,447 income tax appeals cases filed (an average of nearly 900 a year) whereas the High Court of Bombay, in the same period, saw 10,185 income tax appeals (an average of nearly 2,000 a year) filed before the Bombay Bench alone.

———